Morningstar: The Stock, The Characters, and What You Need to Know

The Oracle's Final Bow: Is Anyone Listening?

Warren Buffett, the Sage of Omaha, is finally hanging up his cleats at 95. This isn't just an exit; it's the closing of a chapter, a definitive marker in the annals of finance. For decades, his annual letters and shareholder meetings have been less about quarterly earnings and more about a masterclass in human behavior and enduring principles. As a longtime Berkshire Hathaway shareholder (and yes, an occasional pilgrim to Omaha myself), I’ve always appreciated that. His recent Thanksgiving letter, a final flourish of wisdom, reinforces what many of us already knew: the man’s value far exceeds his balance sheet.

He’s the kind of figure whose aphorisms stick with you, long after the specifics of the OxyChem deal fade into memory. My personal favorite? "Only when the tide goes out do you discover who’s been swimming naked." It's a brutal, elegant truth, and one that feels particularly relevant in today’s frantic market.

I recall watching him, years ago, at an Omaha shareholder meeting, a sea of eager faces before him, patiently fielding a rambling question from a young man in the third row about derivatives—a topic he famously disdained. He just nodded, smiled, and offered a simple, disarming truth, completely unfazed. That’s the essence of Buffett: calm, collected, and utterly grounded. He presented a list of ten virtues, a kind of investment in life itself: kindness, integrity, patience, caution, positivity, independent thinking, humility, contentment, valuing continuity, and practicing gratitude. These aren't just feel-good platitudes; they're the bedrock of a robust, anti-fragile existence, and arguably, a sound investment strategy.

But here’s the rub, the quantitative dissonance that keeps me up at night: while Buffett preaches the long game, the market seems to be playing a hyperactive round of whack-a-mole. We’re seeing over 1,000 new ETFs launch in the U.S. this year alone. That's a staggering number, indicative of a market ravenous for the "next big thing," often at the expense of fundamental rigor. And then there's the weekly parade of newly overvalued stocks, a testament to a different kind of market philosophy entirely.

The Market's Short Attention Span

Let’s talk numbers, because that’s where the rubber meets the road. Morningstar, a name familiar to any serious investor, just flagged 13 Newly Overvalued Stocks this Week, pushing them into 1- or 2-star territory. The broader U.S. market, according to Morningstar’s own index, is hovering at a 10% premium to its fair value estimate on a market cap-weighted basis. A 10% premium isn't a rounding error; it’s a significant lean.

Take Newmont, for instance. It climbed 5.29% in a single week, bumping its Morningstar Rating down to a mere 1 star. Its price now sits a full 42% above its fair value estimate of $62 per share. Not just 'overvalued,' but 42% overvalued, with a Medium Uncertainty Rating. Or consider Valero Energy, up 3.5% in a week, now trading at a 32% premium. The market, it seems, is perfectly content to disregard these red flags, chasing momentum with an almost childlike glee. My analytical mind wants to understand the psychology behind this, but the data simply points to a collective shrug.

Buffett’s famous lament, "Because no one wants to get rich slow," echoes like a prophecy over these weekly lists. The market right now feels less like a careful gardener tending to long-term growth and more like a short-order cook, flipping burgers (stocks) faster than anyone can digest them, hoping for a quick sale before they burn. The underlying methodological critique here isn't just about the accuracy of Morningstar ratings; it's about the market's seemingly willful disregard for them. It’s almost as if the warnings are just background noise in a frenetic trading pit.

And this is the part of the report that I find genuinely puzzling: the sheer volume of new offerings and rapid valuation shifts. When you look at the 1,000+ new ETFs launched this year alone—many with questionable long-term merit, as one Morningstar analyst pointed out—it just screams "action for action's sake." Even the excellent Vanguard Total Inflation-Protected Securities ETF (VTP), charging a minimal 5 basis points, is an outlier in a field often characterized by higher fees and chasing trends.

The Unanswered Questions of Patience and Integrity

Buffett’s lessons on patience, caution, and integrity feel almost quaint in this environment. He once said, "It takes 20 years to build a reputation and five minutes to ruin it." In a market driven by fleeting trends and social media sentiment, is reputation even a primary concern for many participants? Or are we in an era where the immediate gratification of a quick gain overshadows the long-term cost of compromised principles?

His advice to "Ask yourself if you would be willing to have your actions appear on the pages of a newspaper the next day" is a powerful ethical compass. But in the anonymous, high-frequency world of modern trading, how many truly pause to consider that? And when he urged us that "Predicting rain doesn’t count. Building arks does," he was talking about preparedness, about having a "Fort Knox balance sheet." Yet, the pursuit of leverage and speculative plays continues unabated. What happens when the tide really goes out on these newly overvalued names? Will anyone remember the lessons about patience and integrity when the bottom drops out? Or will they simply move on to the next hot thing, leaving the wreckage behind?

The Enduring Irrelevance of Wisdom

Buffett’s retirement marks the formal departure of a titan whose principles were once paramount. Yet, the current market, with its frenetic pace and apparent indifference to fundamental valuation, suggests that his wisdom might be more of an historical artifact than a guiding light. The data paints a clear picture: the market is moving too fast to listen, too greedy to be patient, and perhaps, too short-sighted to truly care.

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

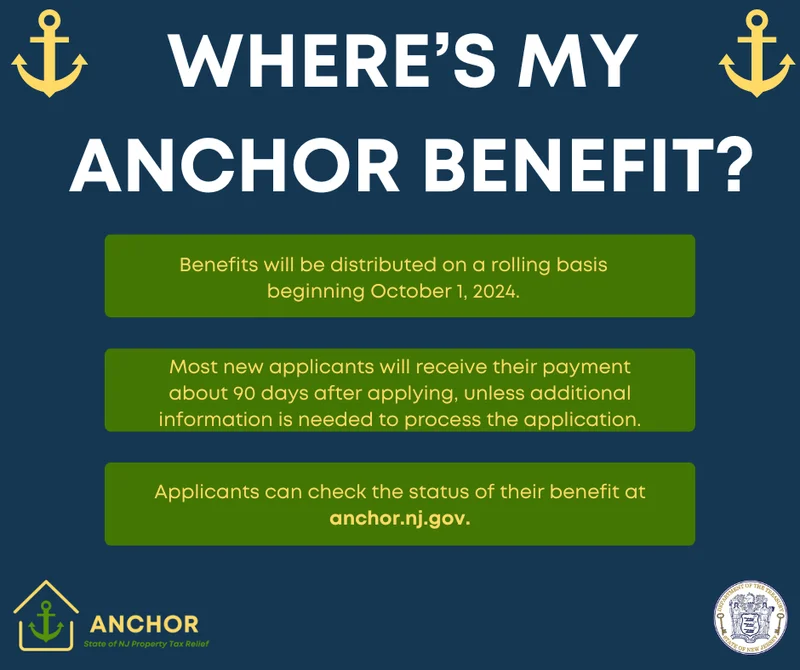

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

- Search

- Recently Published

-

- Barcelona Distances From Crypto Sponsor: A Pivotal Moment for Ethical Innovation

- Oracle Stock: The Bold AI Cloud Bet Igniting a New Era

- Porto's: Is there anything new to care about?

- Oscar Health Stock: Decoding Its Breakthrough Potential

- American Signature Files Chapter 11: What Happened?

- Firo's Price Surge: What's Driving the Rally and Can It Last?

- Morningstar: The Stock, The Characters, and What You Need to Know

- Binance: Its Current State, US Operations, and CZ's Outlook

- Blue Owl: Capital, Stock, & Private Credit Dynamics

- Switzerland: Time Zones, Major Hubs, & Key Logistical Data

- Tag list

-

- carbon trading (2)

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (30)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- PENGU (3)

- Plasma (5)

- Zcash (7)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- SX Network (3)